Dollar Carry Trades Set to Trounce World’s Booming Stock Markets

(Bloomberg) — The dollar is regaining its crown as one of the world’s most appealing assets, defying talk of a “Sell America” trade that had raised troubling questions about the outlook for the global reserve currency.

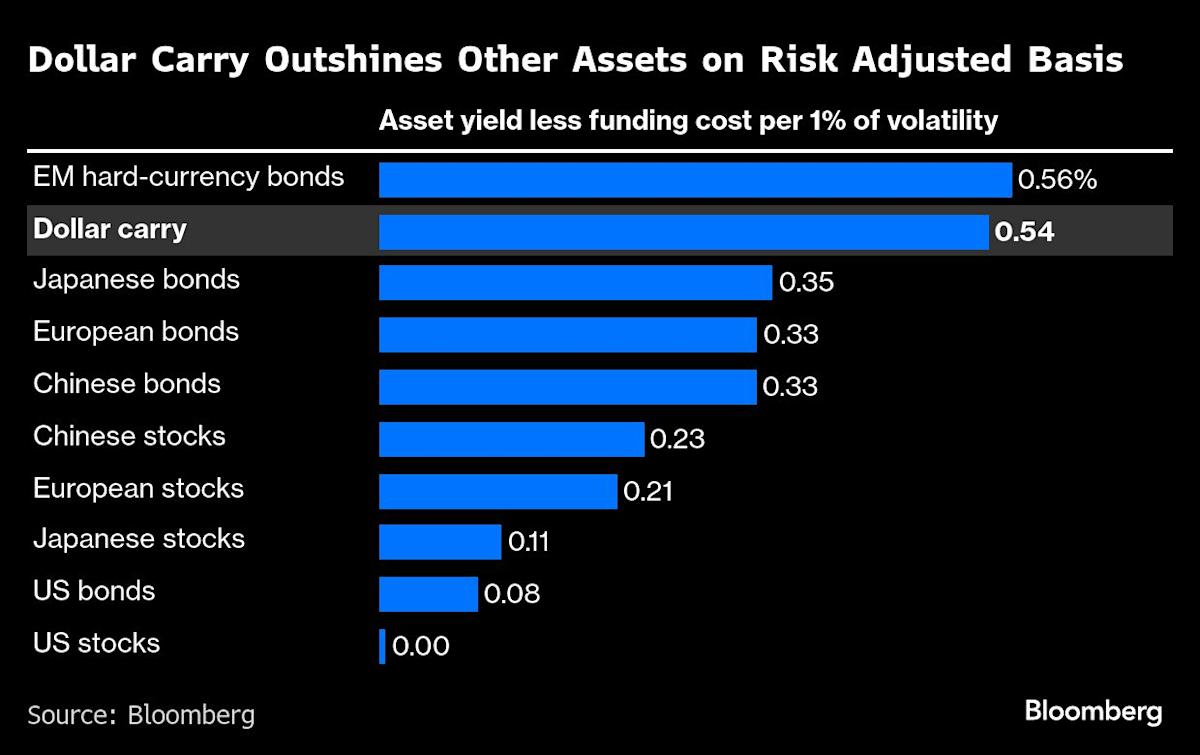

A simple strategy of borrowing in low-yielding currencies like the Japanese yen or the Swiss franc and putting your money in dollars looks set to beat the implied returns on markets such as European stocks and Chinese government bonds once the volatility of these assets is taken into account, according to Bloomberg calculations.

Most Read from Bloomberg

That suggests the dollar will maintain its critical position in global portfolios, despite worries about its future this year as President Donald Trump shook up the global economic order. A Bloomberg gauge of the dollar is down about 7% this year — its worst performance in eight years — but it has bounced back around 3% from a September low, in part because of the so-called carry trade.

“The dollar will end up being one of the highest carry currencies again,” said Yuxuan Tang, a strategist at JPMorgan Private Bank in Hong Kong. “Whether it’s from a directional or carry perspective, it’s still going to be about a strong dollar,” she said.

The implications of the dollar’s renewed appeal for investors can’t be overstated for global markets.

Carry trades can drive massive capital flows, reshaping asset values and influencing sentiment from New York to Singapore. When investors borrow cheaply to chase higher returns elsewhere, liquidity is often amplified — fueling rallies in risky assets that can just as quickly unravel when volatility spikes.

The appeal of dollar carry has been helped by a sharp drop in the greenback’s volatility, in part because a prolonged government shutdown dampened price swings in the $9.6 trillion-a-day global foreign exchange market. That reduces the risk for foreign traders loading up on dollar assets without hedging their currency exposure.

To make the calculations, Bloomberg used earnings yields as a proxy for equity returns; the gap between borrowing rates in yen and Swiss francs and similar-maturity investment yields in dollars to estimate the carry; and bond indexes that capture a range of maturities for yields on government debt. Volatility was calculated for the next month, with option-implied measures used for the currencies and stocks and swaptions for bonds. The exception was in China and emerging-market debt, where realized volatility was used.

Stock Market Fears

The rising appeal of the carry trade comes as investors worry that an artificial intelligence-fueled rally in global stock markets will come to an end. The S&P 500 Index has jumped more than a third from its April lows, while indexes in Europe and China have also soared.

The US equity risk premium, measured as the difference between the S&P 500’s earnings yield and the 10-year Treasury yield, has turned negative. US stocks now offer investors no return whatsoever on a risk-adjusted basis, presuming investors fund their bets by short-term borrowing and pocket a return in line with the earnings yield, the Bloomberg calculations show.

The math is similar — albeit not as extreme — for other markets. Investors buying Chinese stocks and holding for the next month are likely to get returns of just 0.23% per percentage point of volatility on an annualized basis, according to the calculations, versus the 0.54% per percentage point of volatility they could pocket through the low-risk carry trade. Those holding Japanese stocks look set to do even worse.

The Bloomberg dollar gauge was down 0.1% Tuesday in the US trading session after the ADP Research data suggested the labor market slowed in the second half of last month. As the longest US government shutdown on record is on the path to end, markets are choppy awaiting a slew of official data.

To be sure, the bullish dollar carry trade is not without risks. A sudden drop in short-term rates would erode its advantage dramatically. That could happen if the Fed signals faster rate cuts than markets currently expect, hardly a black swan event given the uncertainty over economic data.

“As the Fed may still cautiously reduce policy rates in the near term, the dollar could remain an attractive carry asset,” said Jacky Tang, Deutsche Bank AG’s chief investment officer for emerging markets and head of discretionary portfolio management. “However, there’s uncertainty next year as the Fed may change its pace of rate cuts with the new Fed chair.”

What Bloomberg Strategists Say…

“With yield differentials still wide and funding trades profitable, the carry trade is back in favor.”

Nour Al Ali, Markets Live Strategist

Investors could also get equity returns wildly at odds with earnings yields, which are calculated by dividing earnings per share by the stock price. Although research has found that earnings yields have predictive value for stock returns, short-term market moves can be chaotic — something that few investors need telling after such an unpredictable year.

Still, there’s plenty of hope for dollar bulls looking to ramp up long-dollar carry strategies into 2026.

US inflation of 3% in September, well above the Fed’s 2% target, remains a sticking point for some officials. Fed official Austan Goolsbee recently expressed nerves about inflation, adding that he wants to see more data before deciding how to vote at the Fed’s December meeting. If strong data continues, a slower pace of easing could protect carry returns into next year.

“Dollar carry trades may remain attractive as long as the macro and financial market backdrop remains resilient,” said Aroop Chatterjee, strategist at Wells Fargo in New York.

(Updates with dollar move in US trading in 12th paragraph)

Leave a Comment

Your email address will not be published. Required fields are marked *