(Bloomberg) — Junk bond investors are getting more skittish about risk.

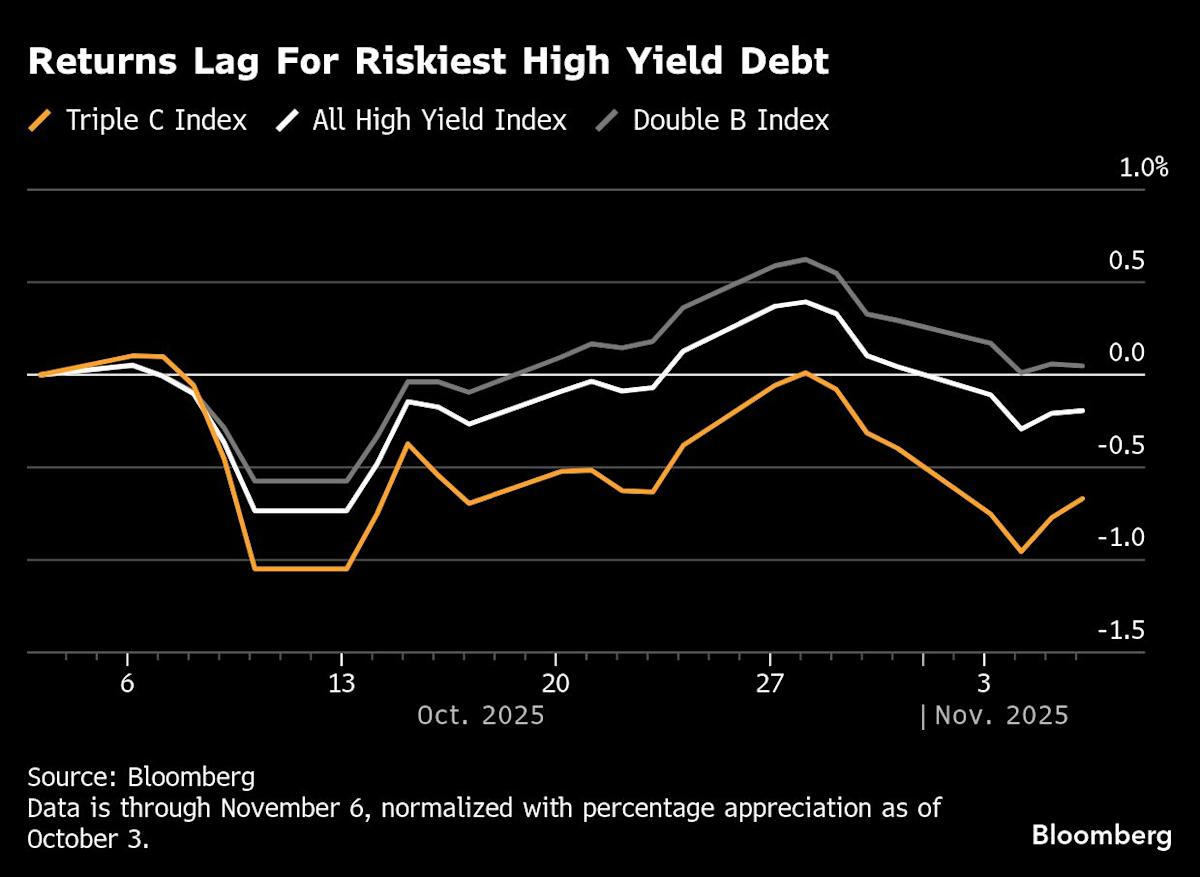

An index of CCC rated bonds in the US has dropped nearly 0.8% over the month ended Thursday, underperforming the broader high-yield market as investors increasingly avoid the riskiest debt. Distressed US dollar loans jumped to $71.8 billion at the end of October — the highest since President Donald Trump outlined his tariff policy in April.

Most Read from Bloomberg

Spreads between US investment-grade bonds and junk have widened over the last week, signaling that investors are favoring safer bonds instead of high-yield notes.

“There is a greater level of caution at the first whiff of potential problems right now,” said Steven Oh, global head of credit and fixed income at PineBridge Investments.

The junk bond market is hardly tanking. Spreads on the securities are still below their average for 2025. For much of the year, high-yield bond spreads have resisted the force of gravity, even as signs of potential trouble emerged. In July, investors were piling into CCC bonds, shrugging off a warning from Jamie Dimon, JPMorgan Chase & Co.’s chief executive officer, that credit spreads were “a little unnaturally low.”

In September, risk premiums on high-yield bonds came close to their lowest levels of the year, even after car parts maker First Brands Group, which had borrowed in the leveraged loan market, filed for bankruptcy amid allegations of fraud. Tricolor Holdings, a used car seller that had borrowed in the asset-backed market, also filed for bankruptcy that month amid fraud allegations.

The latest weakness in junk bonds is a sign that the debt won’t rally forever, particularly for the riskiest securities. Spreads on CCC debt widened about 27 basis points from Oct. 31 through Thursday, compared with 13 basis points on average for all high-yield debt, data compiled by Bloomberg shows. The extra compensation investors demand to hold blue-chip BBB rated bonds compared to more speculative BBs rose 11 basis points over that period.

Some market watchers point out that investors aren’t necessarily avoiding all CCC bonds, but rather credits that have been downgraded to CCC recently, and are on a downward trajectory.

The fact that investment-grade spreads are still close to historical levels of tightness — at 81 basis points as of Thursday’s close — and high-yield spreads aren’t, is a trend to watch, said Mike Schueller, senior portfolio manager at Allspring Global Investments. More consumer-related sectors within high-yield are weakening, like subprime lenders and retailers that cater to lower-end consumers, he added.

Distressed bond supply has “swung wildly” this year, climbing to $100 billion in April from $50 billion in January, according to Bloomberg Intelligence. October marked the second-straight month of increasing supply, hovering at about $72 billion. While still relatively benign, previous breakouts in distressed supply from troughs have signaled the start of a “notable bout of risk aversion,” analysts Philip Brendel and Negisa Balluku wrote.

Meanwhile in the leveraged loan market last month, four deals were shelved, following an August and September that saw six deals pulled. On Thursday, Bloomberg reported that Energos Infrastructure shelved a $2 billion junk-debt sale, as the company owned by Apollo Global Management Inc. struggled to attract investor demand.

Investors also pulled $1.3 billion from bank loan exchange-traded funds in October — the biggest monthly outflow from the sector since April — according to data compiled by Bloomberg Intelligence. Add it all up, and there may be good reason for investors to be more skittish now.

“What sticks out to me is that while the share of distressed debt is small on a historic perspective, it’s quite large compared to prior periods when you’ve had very tight spreads,” said Winnie Cisar, global head of strategy at CreditSights Inc.

WATCH: This week’s guests include BlackRock Americas Chief Investment and Portfolio Strategist Gargi Chaudhuri, Richard Bernstein Advisors Deputy CIO Mike Contopoulos, Vanguard Fixed Income Head of Global Taxable Credit Research Colleen CunniffeBlackRock Americas Chief Investment and Portfolio Strategist Gargi Chaudhuri, Richard Bernstein Advisors Deputy CIO Mike Contopoulos, Vanguard Fixed Income Head of Global Taxable Credit Research Colleen Cunniffe

Click here for a podcast with DoubleLine on risks around the AI debt boom

Week In Review

Alphabet Inc. sold $17.5 billion of bonds in the US, after issuing €6.5 billion ($7.48 billion) of notes in Europe, adding to a wave of borrowing from technology companies as they invest aggressively in artificial intelligence.

Cipher Mining Inc. raised $1.4 billion through a high-yield bond offering to help fund the construction of a data center linked to Alphabet’s Google, the latest example of the AI borrowing boom spilling into the US junk-debt market.

Meanwhile, a group of about 20 banks is providing a roughly $18 billion project finance loan to help fund the construction of a data center campus tied to Oracle Corp.

Global Payments Inc. sold $6.2 billion of bonds to help fund its acquisition of Worldpay Inc., while Berkshire Hathaway Inc. hired banks for a potential yen-denominated bond sale, as borrowers around the world drove issuance this year to a new record.

AI-related borrowing, as well as a growing number of acquisitions, helped push global bond sales to a record $5.95 trillion this year.

The end of an era of essentially free money in Japan, a flurry of dealmaking and the AI boom have unleashed record overseas borrowing by the nation’s firms whose renewed swagger is shaking up global markets.

Country Garden Holdings Co., one of the biggest casualties of China’s real estate crisis, is wrapping up its $14.1 billion offshore debt restructuring after more than two years, with a two-tiered vote of approval from its creditors.

A group of Wall Street banks is considering bringing in private credit firms on a portion of a $12.25 billion debt financing to support Blackstone Inc. and TPG Inc.’s acquisition of medical device-maker Hologic Inc.

UBS Group AG is liquidating two invoice finance funds with exposure to First Brands Group, an early sign of how large financial institutions are dealing with the fallout from the bankrupt auto-parts supplier’s collapse.

First Brands won access to $600 million of remaining bankruptcy financing, which company lawyers said was needed to prevent the company from immediately shutting down.

The share of consumers in the subprime credit risk category has reached levels not seen since 2019, signaling a growing number of borrowers are in poor financial health.

More of the corporate bond market’s angels are losing their wings, with about $42 billion of the notes this year dropping from investment-grade to junk status — becoming so-called “fallen angels,” according to Barclays Plc.

The US SEC has been scrutinizing Egan-Jones Ratings Co., delving into the business practices of a leader in the fast-growing market for private-credit ratings.

Alteryx Inc. is sounding out investors for a new $2.4 billion loan to refinance private debt and provide a special dividend to its private equity owners.

French frozen foods grocer Picard Groupe SAS priced a €280 million ($322 million) note, in what was the first CCC rated offering to hit the European junk bond market since July.

UBS Group AG sold its first bonds since a court decision raised questions about the Swiss lender’s possible exposure to previously canceled Credit Suisse debt.

Telecom company Orange SA sold its biggest-ever bond deal just a week after agreeing to buy out the remaining stake in its Spanish joint venture MasOrange for $4.9 billion.

Pine Gate Renewables filed for Chapter 11 bankruptcy — the latest solar firm to do so amid a pullback of US policy support for renewable energy development.

Lenders are set to take over Canadian broadcaster Corus Entertainment Inc. after reaching an agreement to swap their debt for equity, ending decades of control by the billionaire Shaw family.

New World Development Co. told some creditors during meetings that there’s not much room to sweeten the terms of its $1.9 billion debt swap proposal.

On the Move

Laura Coady joined Blackstone Credit & Insurance as Global Head of CLOs and European Head of Liquid Credit Strategies. She was previously at Jefferies.

Goldman Sachs Group Inc.’s asset-management unit is reshuffling its credit team, promoting Simon Dangoor as the new deputy chief investment officer of fixed income. Three managing directors are joining the global credit team: John McClain from Brandywine Global Investment Management, Alex Karam from Fidelity Investments, and Niels Schuehle from AllianceBernstein.

Goldman Sachs also named David Eisman global co-head of its financial and strategic investors group, as the firm shuffles leadership of the team that works with private equity firms, credit funds and other alternative asset managers.

Ares Management Corp. is looking to strengthen its presence in the Asia-Pacific region and has started a search for a partner-level executive to join its leadership team.

Leave a Comment

Your email address will not be published. Required fields are marked *