Rachel Reeves has every right to be furious with the Office for Budget Responsibility (OBR).

The biggest hole in her plans for public finances come not from Donald Trump’s trade war or from higher interest rates, or even the damage done by her tax raids earlier this year.

Instead, it is a tweak to a spreadsheet which has sent the Chancellor scrambling to find tens of billions of pounds.

The OBR, headed by Richard Hughes, is expected to cut its forecast for productivity growth by as much as 0.3 percentage points when it publishes its latest forecasts next week.

This is a critical number used as a foundation stone for projecting the Treasury’s tax receipts – lower productivity means less predicted output per worker, with lower wages and weaker tax receipts as a result.

In short, it will cost all of us dearly.

The downgrade is expected to blow a near £20bn hole in Reeves’s Budget. Finding that vast sum from tax rises is equivalent to adding 2p to all the main rates of income tax.

The decision is understood to have infuriated the Chancellor, leading to a breakdown in relations between the Treasury and OBR. Reeves, once a champion of the fiscal watchdog, is now counting the cost of its decisions.

In a sense the biggest surprise is not the downgrade, but the fact that it has taken so long to come at all.

For years the watchdog anticipated productivity growth would return to something resembling its pre-financial crisis rate. And year after year, this failed to happen – productivity growth remained painfully elusive.

The OBR in turn pushed back the point at which it expected the recovery to take hold, and cut back the pace of the anticipated acceleration when it did finally arrive.

The looming cut even to these diminished forecasts represents the latest admission of an error in its projections.

The OBR is generally much more optimistic than most other forecasters. This is illustrated by the “hedgehog” chart (displayed at the top of the article) showing the watchdog’s persistent over-estimation of productivity growth.

The Bank of England, for instance, expects productivity in terms of output per worker to grow by 0.8pc next year – well below the OBR’s 1.3pc.

Similarly when it comes to output per hour worked – a slightly different measure – the OBR’s projected increase of 1.1pc is firmly above private sector forecasts.

Berenberg Bank expects a 0.8pc increase, for example, while 0.6pc is pencilled in by Capital Economics and Oxford Economics forecasts just 0.1pc growth.

That a downgrade is justifiable and will bring the OBR into line with other forecasters does not make the move any less painful – either for taxpayers or for Reeves.

She is hardly the first Chancellor to be unhappy with the official bean counters. Kwasi Kwarteng tried to handle his mini-Budget in 2022 without consulting the forecasters, for instance.

The then-prime minister, Liz Truss, has spent the subsequent years arguing the OBR’s forecasts are “fundamentally flawed”.

Sir Mel Stride, the shadow chancellor, has now weighed in on the forecast process and its “integrity” – demanding the OBR spell out when and how it drew up its numbers amid complaints that the Treasury has been selectively leaking forecast to the Chancellor’s benefit.

Meanwhile Paul Nowak, general secretary of the Trades Union Congress, has complained the organisation’s calculations are too sympathetic to spending cuts, undermining Left-wingers’ preferred policies.

Reeves’s frustration with the OBR is a far cry from her initial position to the watchdog on becoming Chancellor. She beefed up its importance as a sign she would follow a prudent fiscal policy.

This included a new “fiscal lock” requiring the OBR’s opinion on any tax or spending policy worth more than 1pc of GDP, around £30bn.

The aim was to highlight the difference between Labour and the tarnished Tories, and to reassure voters Labour could be trusted with the economy.

Instead, she feels the rug has been unfairly pulled from under her feet.

The Chancellor has said privately she wished the OBR had made this move a year ago, allowing her to deal with the productivity issue as part of the record-breaking tax rises in her first Budget.

Simon French, chief economist at Panmure Liberum, says he has “sympathy” with the Chancellor.

“There are two moving parts to the Budget. The productivity part, which sums to £15bn to £20bn, is not really her fault. This is a 20-year drag, with decisions made by her predecessors,” he says.

“Then there are the policy U-turns on the winter fuel payments, PIP and the two child benefit cap. That is her party’s fault. She is right to be furious on one element of the loss of headroom. But she should be equally furious with her own side.”

James Smith, an economist at the Left-leaning Resolution Foundation think tank, says the timing of the downgrade is particularly unfortunate.

“It has been obvious for a while that the OBR has been in the wrong place on productivity. But if you look at the productivity data over the past year or so, they have been quite strong,” he says.

“So the timing is doubly baffling in a way, because not only has it taken a long time for the repeated disappointments on productivity to feed through into a different [forecast] assumption, but we actually have quite strong productivity right now.”

The downgrade comes with a political slant, too: the Conservatives benefitted from the OBR’s overoptimism on productivity.

If this had happened two years ago, Jeremy Hunt would not have been able to offer his pre-election cuts to the National Insurance contributions paid by workers. Now Reeves has to find the money to fill the gap.

Productivity might be the biggest moving part in the Budget, but it is not the only one.

While those forecasts are moving against the Chancellor, the OBR said interest rates in markets are moving in her favour.

This represents a blessed relief for Number 11– as interest rates just a few months ago were at painfully high levels, draining the Exchequer of cash.

The Government is already spending more than £100bn per year servicing the national debt, which is on track to rise above £3 trillion.

The OBR forecasts how much interest will be paid in future years in part based on conditions in financial markets.

Officials decided last week to switch the “window” for taking this data from markets, moving it from the 10 days to Oct 10 to the 10 days to Oct 21.

That means the forecasts will now include lower borrowing costs, potentially saving the Chancellor £1.7bn in projected interest costs. Such a move does not wipe out the impact of lower productivity, but helps ease the blow.

It also shows just how sensitive the finances can be to the choices of the OBR’s officials.

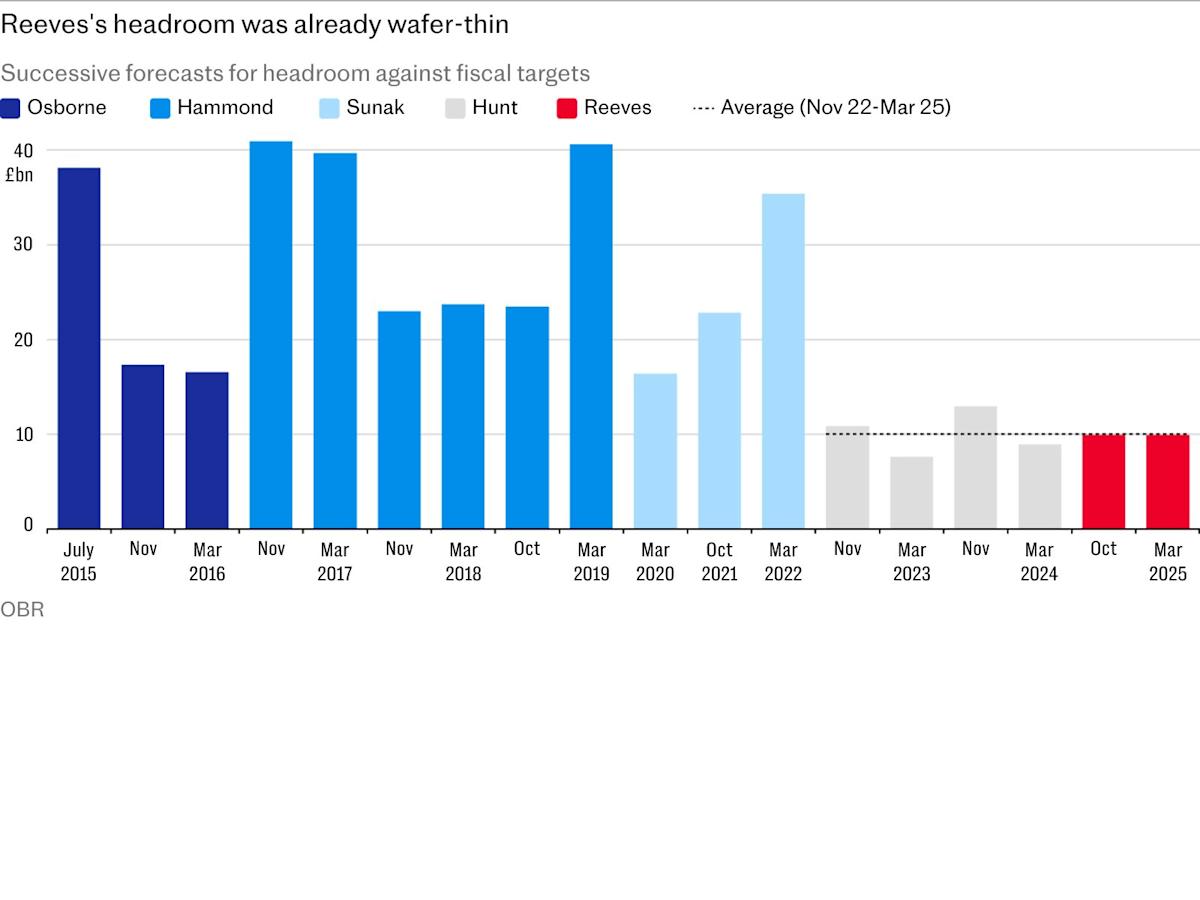

This sensitivity is heightened by Reeves’s decision to leave herself so little headroom after her first Budget and the Spring Statement.

Chancellors in the past typically kept a buffer of around £30bn, providing some insulation against unfavourable economic developments.

Hunt, the final Conservative chancellor, cut this to £10bn and Reeves kept that steady – even as she ramped up spending and borrowing with a new set of fiscal rules.

Back in March, Hughes pointed out the dangers of running with such little leeway.

Sir Charlie Bean, a former member of the Budget Responsibility Committee, which heads the OBR, says the risks should have been clear to Reeves.

“This was always a risk, and frankly she was foolish in the Budget a year ago to leave herself so little headroom,” he says.

“Forecasts are inherently uncertain. It always makes sense to have a pretty sizeable room for error built in.”

b’

Reeves\’s headroom was already wafer-thin

‘

He notes that views on future productivity abound, ranging from techno-optimists who think nanotechnology or artificial intelligence will save the day, to those who fear the great bounds of human progress are now behind us with little reason to expect the current slump to come to an end.

As a result, forecasters sensibly “hedge their bets” and choose a path somewhere between old rates of growth and recent rates of stagnation. The exact slope of that path merely varies as officials reassess recent history.

Critics argue that the combination of weak growth and little headroom make the OBR effectively the arbiter of all policy decisions, as it assesses the impact on the Government’s ability to hit the fiscal rules.

This, goes the argument, is undemocratic and hands the watchdog far too much power.

Sir Charlie dismisses this argument as “complete nonsense”.

“The OBR is a calculating machine. It cranks the numbers,” he says. “The Government chooses the fiscal objectives and how it wants to be evaluated against them. It chooses how much room it wants to leave itself, it chooses all the fiscal measures.

“The OBR doesn’t insist the Chancellor changes the policy if they are not meeting whatever objectives they have set themselves.”

Yet the OBR’s sway is undeniable. Leaving so little headroom risks distorting incentives, as politicians seek to find policies that will be scored favourably by the Budget watchdog, says Yael Selfin, chief economist at KPMG. Voters’s concerns may end up being a distant second.

“Such a narrow buffer risks skewing policy decisions to ensure fiscal rules are met in the short term rather than putting emphasis on the longer term gains for the economy and society,” Selfin says.

Treasury insiders stress the OBR’s independence to make such forecast changes is a key part of Britain’s economic framework, which is designed to make fiscal policy more credible.

Fundamentally, the problem is that forecasting is tough and events have not transpired as economists predicted – nor as politicians would have liked.

Productivity did not rebound rapidly after the financial crisis, and has spent the past 15 years performing extraordinarily poorly by historical standards.

Britain, and much of the G7, have struggled to grow their productivity.

Last year average output per hour worked in France and Italy was lower than its 2019 level, according to the OECD, while in Britain, Germany, Japan and Canada it had barely risen in five years.

Yet the US has proved this need not be our fate. Productivity in the world’s largest economy grew by almost 10pc over the same period, wiping the floor with the rest of the rich world.

French, at Panmure Liberum, says that after years of self-inflicted pain, including “mad energy policies” and disruption such as Brexit, salvation on productivity could come in the form of widespread adoption of artificial intelligence.

On some metrics, productivity is on the up. The downgrade comes from old data – it is “all rear-view mirror stuff”, says French.

If that is right, the OBR downgrade might be coming at precisely the wrong moment.

The painful tax rises precipitated by the forecaster’s change of heart may end up being totally unnecessary, meaning one damaging forecast error is replaced with another.

Leave a Comment

Your email address will not be published. Required fields are marked *