New Crypto Deals Put Retail at Risk After $17 Billion Wipeout

(Bloomberg) — Executives are turning to a novel structure to fund crypto accumulation vehicles as investor appetite thins.

They’re called in-kind contributions, and they now account for a growing share of digital-asset treasury, or DAT, deals. Instead of raising cash to buy tokens in the open market, DAT sponsors contribute large slugs of their own crypto, often unlisted and hard to value.

Most Read from Bloomberg

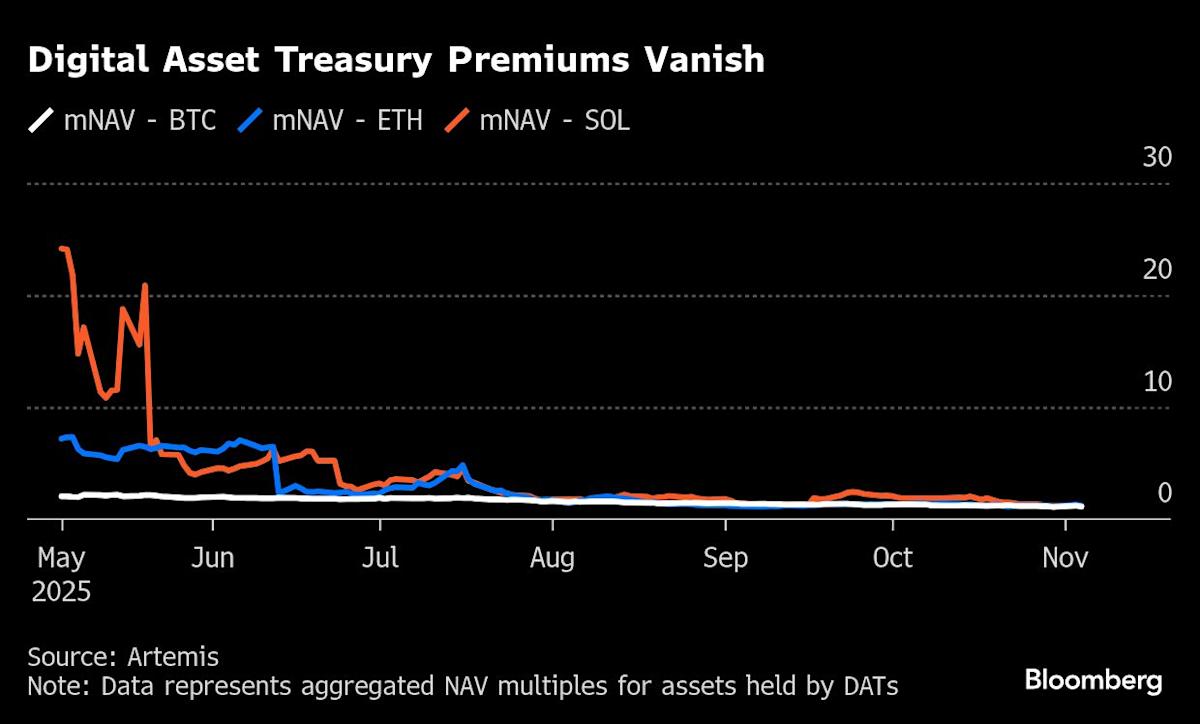

Digital-asset treasuries are a new breed of public company built to hold concentrated crypto positions. The structure surged in 2025 as small-cap firms, especially in biotech and mining, reinvented themselves as digital-asset proxies. Sponsors provide tokens or raise money to buy them, and the stock then trades as a kind of listed bet on crypto. For insiders, it’s a shortcut to liquidity. For investors, a wager on upside.

But not all DATs carry the same level of risk. Earlier deals raised money to buy tokens through regular markets, which offered at least some independent price check. In-kind contributions skip that step — letting insiders decide what their tokens are worth, sometimes before the token even trades publicly. That shift means pricing and trading risks land more squarely on shareholders, many of them retail investors.

Investor faith is already wobbling, with Bitcoin’s latest plunge well below $100,000 adding to the stress. Many DATs that once traded above the value of their holdings now trade below it. As insiders supply the tokens and set their price, it’s becoming harder for investors to tell what these deals are really worth, or when to get out.

The in-kind structure was on full display in a recent $545 million private placement by Tharimmune Inc., a biotech firm-turned-crypto proxy, to set up a buyer of Canton Coins. About 80% of the raise came in the form of unlisted Canton tokens, priced at 20 cents each, according to an investor presentation seen by Bloomberg News. The token began trading on exchanges Nov. 10 and is now around 11 cents, CoinGecko data show.

Tharimmune didn’t respond to a request for comment.

More deals are following the same template. In these placements, insiders contribute tokens — sometimes illiquid or unlisted — to form a treasury, lock in valuations and seed the perception of market demand. But when tokens list below deal price, public shareholders absorb the difference.

The rise of in-kind DATs highlight a broader shift in how crypto risk is being offloaded. With fresh capital harder to attract, sponsors are using public wrappers to crystallize token value and initiate price discovery. The vehicles can resemble circular trades, where the same actors supply the asset, set its value and benefit from the optics of a successful raise. What looks like market demand can instead be recycled inventory.

A sharp market selloff of the kind that occurred in October can leave retail investors bearing the brunt of in-kind trades unwinding.

“Ultimately, if market sentiment shifts, public investors in the fund, particularly retail, may be left exposed if the underlying illiquidity is finally tested, leaving them to absorb the very losses the sponsor’s contribution structure was designed to sidestep,” said Chris Holland, partner at Singaporean consulting firm HM. Especially for smaller tokens, an in-kind contribution “shifts much of the liquidity and market impact risk to the DAT,” he added.

Singapore-based 10X Research said in an October report that retail traders had lost an estimated $17 billion buying stocks modeled on Michael Saylor’s archetypal Bitcoin buyer Strategy Inc.

Canton isn’t alone in leaning heavily on untested tokens to get a treasury deal done. Alt5 Sigma Corp. raised $1.5 billion in August to invest in tokens issued by World Liberty Financial, a crypto venture with ties to US President Donald Trump. Half of the total sum came in the form of WLFI tokens priced at 20 cents each. At that time, WLFI tokens weren’t trading on exchanges.

Then there’s Flora Growth Corp., a Nasdaq-listed company that announced a $401 million deal to start acquiring Zero Gravity tokens in September. On closer inspection, the firm had raised just $35 million in cash to pair with a $366 million in-kind contribution of then-unlisted 0G tokens. Those tokens were priced at around $3 a piece; they subsequently listed, and are now trading at about $1.20.

Flora Growth remains confident in the potential of DATs “to give investors new on-ramps into crypto,” Chief Executive Officer Daniel Reis-Faria said. “I have a long-term conviction-driven approach and belief in both 0G and decentralized AI infrastructure.”

Both companies’ shares have been under pressure from the moment they became crypto proxies. They are each down more than 65% since announcing plans to adopt a DAT strategy.

Alt5 Sigma didn’t respond to a request for comment.

“An 80% in-kind DAT is effectively a thin equity wrapper around one single volatile token,” said Akshat Vaidya, who has overseen investments in crypto treasuries as co-founder and managing partner of Arthur Hayes’ family office Maelstrom. “If the token drops 50%, the share price falls 80%-100% because the premium evaporates at the same time that forced sellers hit the bid.”

Leon Foong, managing partner at Mythos Venture Partners, an active investor in DATs, said that in-kind contributions create “a reflexivity which can act both ways — on the upside but also a downward spiral.” The more illiquid the token, the riskier the deal, he added.

To be sure, in-kind contributions have been part and parcel of the DAT trade since it took off in the first half of the year. In July, crypto veteran Adam Back’s Blockstream poured 25,000 Bitcoin — worth about $3 billion at the time — into a blank check company that partnered with an investment vehicle backed by Cantor Fitzgerald to form a treasury company. But that kind of structure hasn’t raised eyebrows, thanks in part to how liquid and widely distributed the original cryptocurrency has become.

Contributions of less-liquid tokens, on the other hand, create “a very delicate balance,” according to Vaidya, “because the DAT sponsors are usually the same people who hold the most of the underlying token as well.”

(Adds fresh market context in fifth paragraph, updates second chart)

Leave a Comment

Your email address will not be published. Required fields are marked *