BOE Set to Hold Rates as UK Budget Looms Over Decision

(Bloomberg) — The Bank of England is expected to skip an interest-rate cut on Thursday, further slowing the once-a-quarter pace to policy easing that it’s maintained for more than a year.

Investors and economists expect the BOE’s Monetary Policy Committee to leave rates on hold at 4% with UK inflation running at almost double its 2% target and the autumn budget looming on Nov. 26.

Most Read from Bloomberg

A vote for unchanged borrowing costs would end the pattern of reducing rates at every other BOE meeting since August 2024, and contrast with the US Federal Reserve, which loosened policy again on Wednesday.

The pause may be short-lived, though, with traders having ramped up bets on a December cut after weaker-than-expected inflation, jobs and output data. While investors still only see a small chance of a cut in the coming week, the prospect of a reduction on Dec. 18 has risen to almost 60%.

Governor Andrew Bailey has warned that the exact timing of the next rate cut is uncertain, not least because Thursday’s meeting comes just three weeks before Chancellor Rachel Reeves delivers her crucial budget.

Reeves was blamed for fueling increases in food costs after increasing payroll taxes for employers in April. However, another round of hefty tax increases, potentially this time aimed at households, could act as a further dampener on a subdued economy.

What Bloomberg Economics Says:

“A slew of softer-than-expected data in recent weeks has created more uncertainty about the outcome of this wee’s meeting. A cut is possible, but with rates close to neutral and inflation still nearly double the BOE’s target, we think a hold is more likely. The central bank will also want to know the contours of the budget before delivering further easing. We remain of the view that rates won’t be cut again until the BOE sees a clear downtrend in the inflation data, likely by April. The risks are tilted toward an earlier reduction — either in February or possibly this December.”

—Dan Hanson and Ana Andrade, economists. For full preview, click here

Elsewhere, central banks from Australia to Sweden to Brazil are likely to keep rates on hold, while Mexican officials may deliver a cut. The US federal shutdown might continue to disrupt data releases there.

Click here for what happened in the past week, and below is our wrap of what’s coming up in the global economy.

US and Canada

Federal Reserve Chair Jerome Powell on Wednesday cautioned against assuming the central bank will cut again in December. In the coming week, a number of Fed officials will offer their own views.

Fed Governor Lisa Cook is set to discuss the economy and monetary policy at an event on Monday. Later in the week, Alberto Musalem, John Williams and Stephen Miran are slated to speak at separate events. Investors will parse their views of the economy and job market given official data releases remain delayed by the month-long government shutdown.

Private-sector reports, meanwhile, will offer clues on the health of the job market. Figures due on Wednesday from ADP Research are projected to show a modest increase in October private employment after declines the prior two months.

The following day, the outplacement firm Challenger, Gray & Christmas will release a count of announced job cuts for October. Those data come after several large companies — including Amazon.com Inc. and United Parcel Service Inc. — announced reductions in headcount.

Other hints about the labor market will surface in the Institute for Supply Management surveys of manufacturers and service providers.

Turning north, Canadian Prime Minister Mark Carney is about to release his government’s first budget, which is expected to slash operating spending while investing heavily in capital projects to grow the economy.

Economists predict the deficit to rise to at least C$70 billion ($50 billion), or more than 2% of gross domestic product. Businesses are hopeful Carney’s push to unleash private capital will include favorable corporate tax changes.

The document, due Tuesday, is also expected to contain a “climate competitiveness strategy” that de-emphasizes emissions targets, plus an immigration plan that aims to scoop up tech talent spurned by US President Donald Trump’s H-1B visa changes.

A day before the budget is unveiled, Bank of Canada Governor Tiff Macklem will participate in a fireside chat hosted by The Logic, a tech publication.

And at the end of the week, jobs data for October is likely to show continued softness after the country shed a net 45,900 positions in the third quarter and the unemployment rate rose to 7.1%.

Asia

November kicks off with a raft of factory activity releases that offers a snapshot of how the region’s export engines are holding up amid global trade strains.

Readings from China, India, South Korea, Taiwan and Japan will be closely watched for signs that supply-chain disruptions and weak external demand are weighing on manufacturing sentiment.

Southeast Asian economies from Indonesia to Malaysia to Thailand also report manufacturing PMIs, with Asean nations risking fewer benefits from Washington’s latest trade deals than the US gains in return.

Indonesia, Vietnam, Taiwan and China also publish trade figures that will show how regional exports are faring in the face of higher US tariffs.

On Monday, Indonesia reports trade and inflation figures. Australia’s data pulse quickens with building approvals, home-price and household-spending releases — a prelude to the Reserve Bank of Australia’s policy decision the next day.

The RBA’s rate-setting board is set to hold the cash rate at 3.6% on Tuesday. Governor Michele Bullock is unlikely to offer firm guidance as policymakers weigh whether sticky prices warrant a longer hold, or if a softening labor market could justify more easing.

The same day, South Korea publishes inflation data. New Zealand reports its quarterly employment and wage figures on Wednesday, and Indonesia releases third-quarter GDP, with economists predicting a slowdown. Singapore posts retail sales for September.

Thursday brings a policy update from Bank Negara Malaysia, which is expected to keep its overnight rate at 2.75%.

By Friday, China’s inflation gauges are expected to show continued disinflation. A series of foreign-reserve updates across the region, including from China, India and South Korea, will round off the week, offering a glimpse into how central banks are managing currency volatility amid a firm US dollar.

Meanwhile, Japan delivers a heavy run of data including labor cash earnings, household spending and real wages — key inputs for the Bank of Japan’s assessment of wage-driven inflation.

Europe, Middle East, Africa

The week will busy in the region for central banks other than the BOE, too. Here’s a snapshot of decisions on the calendar:

Sweden’s Riksbank is widely anticipated to keep its rate at a three-year low of 1.75% on Wednesday. Policymakers have cut borrowing costs by 225 basis points since May 2024 and are now expected to stand pat until late next year amid signs that an economic recovery is building and above-target inflation is easing.

Poland’s central bank may also stay on hold the same day, taking a pause after a series of cuts as inflation eases. Fresh projections are likely to offer guidance on future moves.

On Thursday, Norwegian policymakers are set to keep their key rate at 4%, in line with a more cautious rate outlook after a quarter-point cut in September. While underlying inflation has eased, it’s still clearly above target. Most economists expect no further reductions until the second quarter of 2026.

The Czech central bank, also on Thursday, will probably leave rates unchanged as officials present quarterly economic forecasts.

Following the European Central Bank’s decision to keep borrowing costs steady, several officials are scheduled to speak. Among them will be President Christine Lagarde on Tuesday and Executive Board members Isabel Schnabel and Philip Lane on Thursday. In between, the ECB will publish its wage tracker on Wednesday.

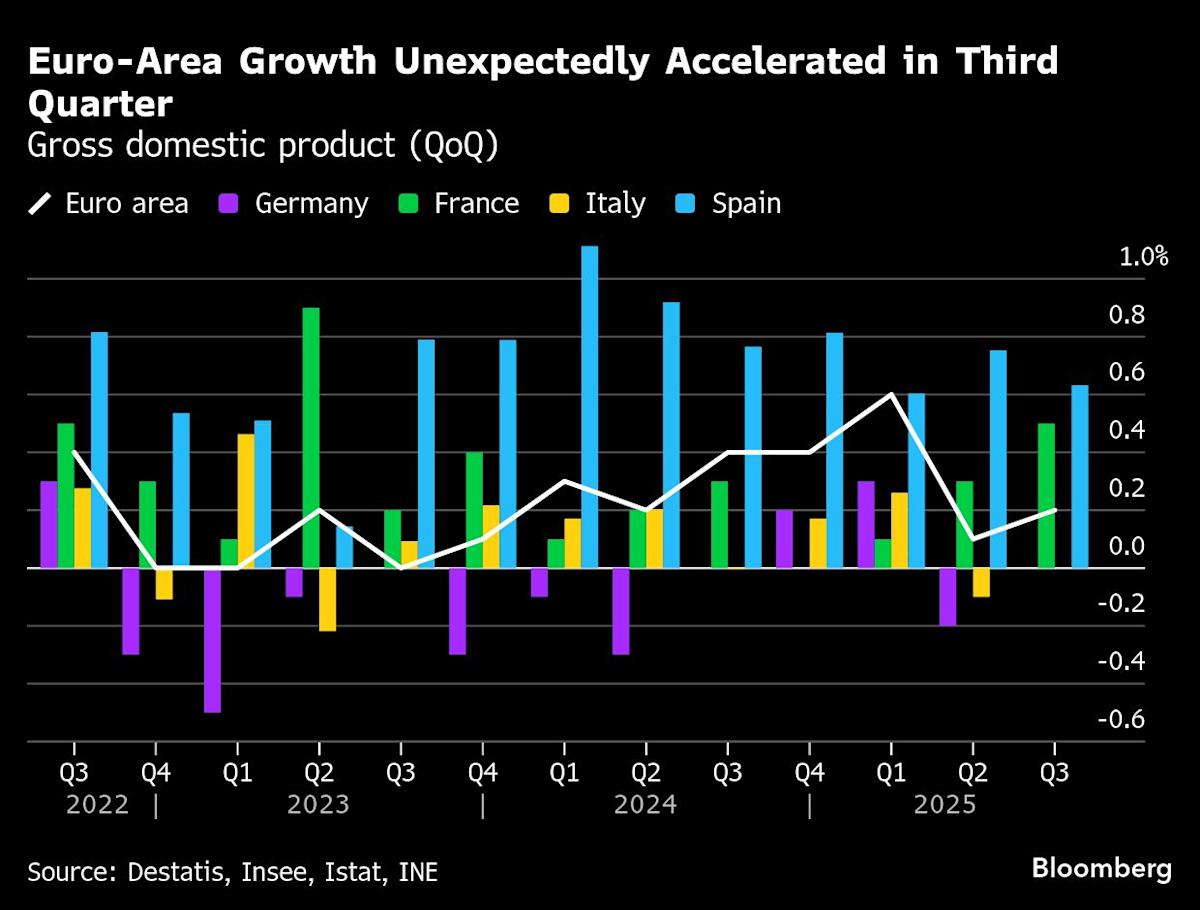

Data in the euro zone will reveal more about the strength of manufacturing at the end of the third quarter following numbers that showed a split, with bumper growth in France and Spain offset by stagnation in Germany and Italy.

German factory orders, production and export statistics for September will be released on successive days starting on Wednesday. French industrial and trade data are also due, as are Spanish manufacturing numbers.

Turning to Switzerland, inflation on Monday will show if price pressures have picked up at all, in line with the Swiss National Bank’s expectation, after three months of just 0.2% consumer-price growth.

Data due on Monday will likely show that Turkish monthly inflation remained above 2% in October, challenging the central bank’s efforts to meet price targets, while annual price growth stayed above 30%. Governor Fatih Karahan will present the year’s final quarterly outlook on Friday, when he’ll also take questions from economists and reporters.

Tuesday may see Madagascar, which recently changed its government after weeks of so-called Gen Z protests, lower its key interest rate from 12% as inflation continues to slow.

Uganda on Thursday will probably leave its benchmark policy rate at 9.75% for a fifth time in a row to get a better grasp of the inflation trajectory.

Latin America

On most occasions, a Brazilian central bank rate meeting sucks the oxygen out of the room, relegating everything else on the regional calendar to second fiddle.

But this is not one of those times: there’s no chance the BCB does anything but hold at 15% for a third straight meeting, and it’s unlikely to offer up any substantive tweaks to current forward guidance.

Argentina, fresh off the resounding win for President Javier Milei’s party in the Oct. 26 mid-terms, posts tax revenue, construction and industrial production data, along with the central bank’s market readout.

Look for the recent deterioration in inflation expectations to at least partially reverse with Milei and his agenda enjoying a new lease on life.

Chile clears the deck for the first round of its presidential election, set for Nov. 16, with trade, copper exports, GDP-proxy figures and October inflation readings. The headline print likely slowed to within policymakers’ 2% to 4% target range.

Banxico appears to be facing an easy call at Thursday’s meeting. Trump has kicked the tariff can down the road again, flash data show LatAm’s No. 2 economy shrank in the third quarter, and inflation — already in the target range — is expected to have slowed last month.

Putting all that together greenlights a 11th straight rate cut, all but certainly a quarter-point trim, to 7.25%.

Colombia’s central bank will issue minutes from its Oct. 31 decision to hold at 9.25% for a fourth straight meeting, as well as the quarterly monetary policy report, which may raise the 2025 GDP estimate and inflation projections as well.

–With assistance from Swati Pandey, Laura Dhillon Kane, Vince Golle, Monique Vanek, Robert Jameson, Mark Evans, Charlie Duxbury, Ott Ummelas and Carla Canivete.

Leave a Comment

Your email address will not be published. Required fields are marked *