Fewer but larger transport M&As in Q3: Study

In the third quarter of 2025, the transport sector witnessed a continued decline in merger and acquisition (M&A) activity, marking the third consecutive quarter of reduced deal volume.

This downward trend, as reported in AlixPartners’ Transport M&A Review, reflected a broader pattern of economic caution driven by persistent geopolitical uncertainties and the pressures of aggressive U.S. trade policy.

Overall, Q3 saw deal volume fall approximately 18% from the previously challenging quarter, and a significant 47.1% drop compared to the same period in 2024. This contraction occurred despite the occurrence of high-profile transactions headlined by the proposed $89 billion railroad mega-merger of Union Pacific (NYSE: UNP) and Norfolk Southern (NYSE: NSC). Excluding this exceptional deal, the total invested capital saw a noticeable decline, further underscoring the subdued M&A environment.

Strategic acquisitions came to the fore during this period, as investors shifted focus towards market consolidation and capability-driven acquisitions to maintain competitive edges amid geopolitical headwinds. The freight transport sector, in particular, experienced notable underperformance. Ongoing capacity growth in road transport led to lower freight rates, while ocean carriers struggled with only marginal recovery in spot rates insufficient to offset deteriorating profitability margins.

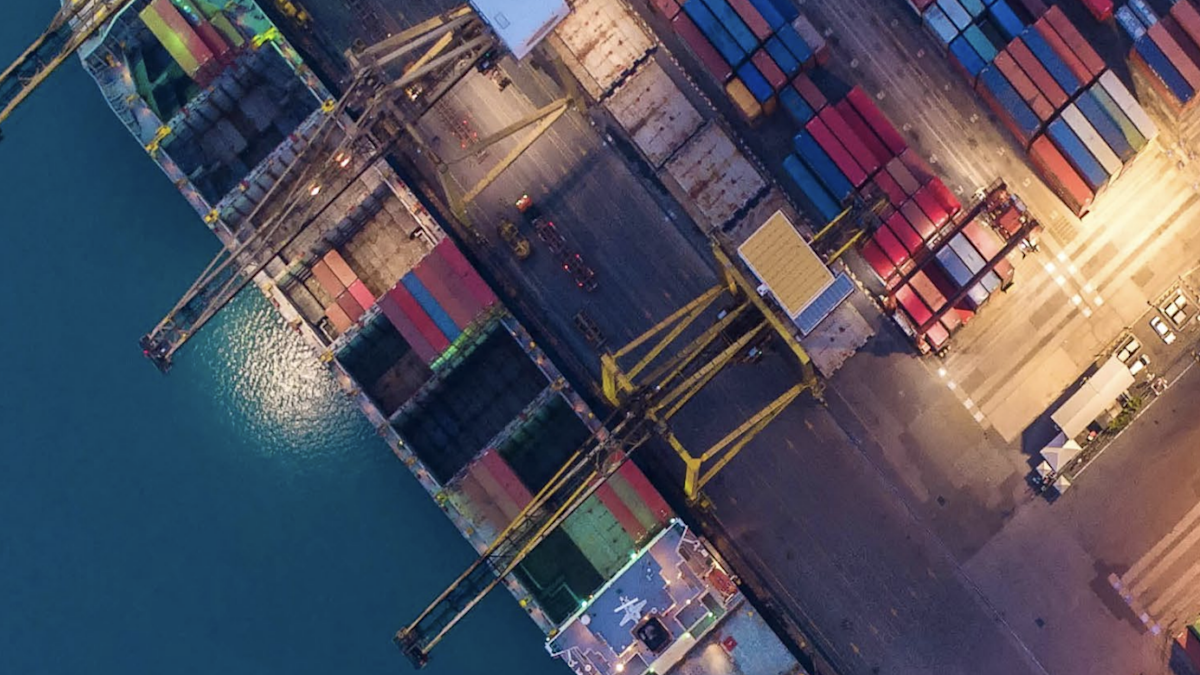

Despite these challenges, ports and infrastructure emerged as one of the few resilient segments within the transport M&A landscape. A consistent strategic interest in ports and associated assets was fueled by localization of supply chains and bolstering of national infrastructure resilience through long-term investments. These moves highlighted the necessity to adapt logistics frameworks to shifting global trade dynamics.

On a regional level, transport M&A remained notably cautious across North America and the Asia-Pacific (APAC) regions. Although these areas registered fewer deals compared to Europe, Middle East, and Africa (EMEA), North America and APAC reported more larger-ticket transactions, signaling a strategic recalibration towards scale acquisitions in the face of ongoing economic pressures. This regional cautiousness was exacerbated by factors such as delayed rate cuts, persistent inflationary pressures and uncertainty within the global freight environment.

Looking ahead, the M&A outlook for the transport sector is characterized by a mix of cautious optimism and strategic maneuvering. Investors are expected to continue navigating alternative deal structures – such as minority stakes and continuation vehicles – to bridge valuation gaps in an effort to preserve flexibility in timing. Recent nominal rate cuts by major central banks have been anticipated to shore up multiples and re-open leveraged deal opportunities, although the precise timing and scale of these opportunities remain indeterminate.

Leave a Comment

Your email address will not be published. Required fields are marked *